Has the splendid economic recovery after the pandemic been dominated by profits rather than wages? The answer to this question has profound consequences for the future direction of the Indian economy.

Two recent data releases from the government provide useful information on this issue. First is the new report of the Periodic Labour Force Survey (PLFS) for 2023-24.

This document provides far more detailed data on wages than the more limited information that many in financial markets track, either on rural wages or wages paid by listed companies.

The problem is that PLFS data is available only once a year, while other types of wage data is available more regularly, and is thus more useful for investors and analysts.

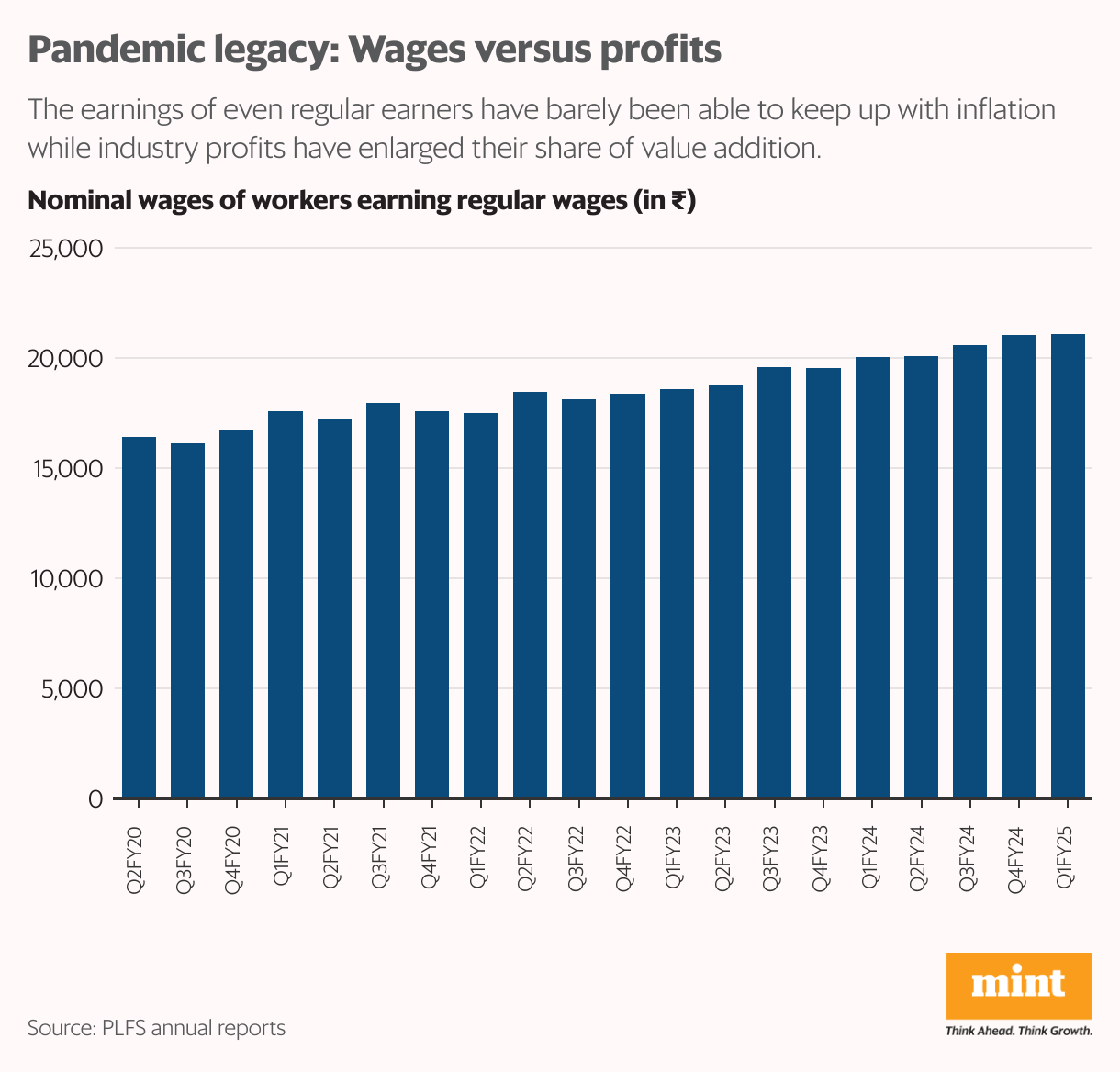

The PLFS annual report provides data on wages of various types of workers across Indian villages and cities. Here, I have only considered the earnings of workers in rural as well as urban areas with regular wages or salaries, rather than other categories such as casual labourers or the self-employed.

The earnings of these workers have generally barely kept pace with inflation over the past five years. They have grown at 5.4% since 2018-19, which has barely kept pace with consumer price inflation.

Wage growth since the end of the pandemic has been slightly better at 6.4%, but still modest when compared to average inflation over the same period.

There are two other categories of workers in India—casual labourers and the self-employed. They get to work fewer hours per week on average, and have erratic earnings.

Those with a regular wage or salary are thus the more privileged part of the Indian labour force, and though their average monthly salary in the fourth quarter of 2023-24 was a modest ₹21,103, it was still better than the ₹433 earned per day by a casual labourer and ₹13,900 by a self-employed worker. So workers with regular monthly earnings are more likely to be discretionary consumers than those in the other two categories.

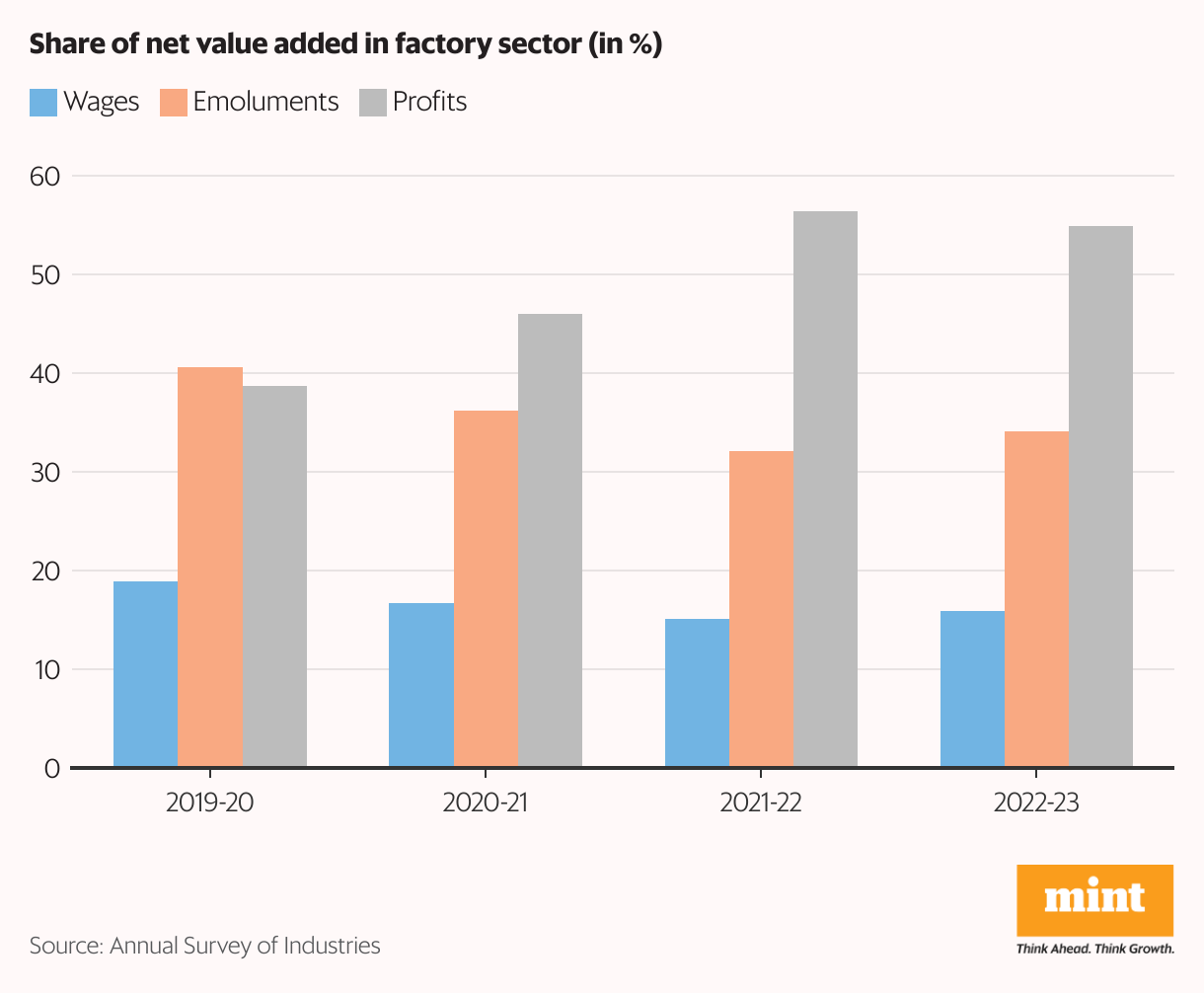

The second bit of useful data comes from the new Annual Survey of Industries (ASI). It shows that the share of labour in net value added (NVA) in the organized factory sector has been slipping.

The survey collects data from factories that have registered under the Factories Act 1948, and specifically factories with electricity that employ 10 workers or more and those without electricity that employ 20 workers or more. So ASI data is restricted to relatively larger units by Indian standards.

Business Standard reported last week that the wage share in NVA is lower than what it was before the pandemic brought the world to a standstill in early 2020. Wages and emoluments cover all payments to workers on the factory floor as well as administrative and managerial employees of a firm.

The flip side of a lower share of labour income in NVA is a higher share of profits. This indicates that the post-covid recovery has indeed been led by profits rather than wages, something that this column had flagged twice in the early quarters of the recovery.

The data made available this month in the PLFS annual report as well as the ASI offers compelling evidence that Indian economic growth since the pandemic has been powered by profits rather than wages. What does this fact mean for the future direction of the economy?

Much depends on the context. Wages have a unique dual role in an economy. First, they provide most households with the income that is needed to buy stuff. So wages power the spending of households.

Second, wages are also a cost for firms. Higher wages can either eat into the profits of firms or make them raise prices if they have the market power to do so.

In other words, the rate at which wages are increasing has implications for consumer spending as well as inflation.

How value added is split between the two main factors of production—labour and capital—also has implications for economic growth. Once again, much depends on the underlying context. Neither profit-led nor wage-led growth is good or bad by itself.

A higher share of wages can actually spur the economy when there is excess capacity in factories. But growing wages can lead to higher inflation in case there is no slack in the economy.

A higher share of profits can be helpful when companies need cash to invest in new production capacity. But companies will prefer to use their higher profits to pay off loans or invest in financial assets in case there is no compelling case to build new capacity in a slack economy.

In other words, whether an economy—and specifically domestic private-sector demand for either consumer goods or machines—benefits from either a wage-led or a profit-led phase of growth depends on the overall slack in the economy.

In India right now, there are signs of weakening consumer demand because of anaemic growth in the wage share, while companies facing excess capacity or fearing Chinese imports are not pouring money into new factories. The story of factor shares in the Indian economy since the pandemic tells us a lot about the economic situation in India right now.

Aadya Jain has contributed to this article.

#Evidence #grown #economic #recovery #led #profits #wages